- September 6, 2021

- Posted by: admin

- Category: BitCoin, Blockchain, Cryptocurrency, Investments

A glimpse at what MicroStrategy could be worth given various scenarios relating to the bitcoin price.

This article will explore:

a) How we might discern the value of MicroStrategy (MSTR), a company in a fairly unique situation in the space, as well as the basics of how value investors operate.

b) Whether or not, given that MSTR is so heavily invested in bitcoin, the main opportunity cost of investing in MSTR is owning an equivalent amount of bitcoin. Hence, why it now makes more sense to value it in bitcoin than in dollars. The explanation is followed by some rough attempts to do just that!

c) Why the approach of pricing in bitcoin might become more and more relevant in the future.

As is well known, MSTR is a company which now has significant skin in the Bitcoin game. In August 2020 it was announced that they were adopting Bitcoin as their primary treasury reserve asset. They converted their entire corporate treasury into bitcoin and have continued to convert free cashflows into bitcoin since. There were also two convertible debt issues to follow, the proceeds of which were also fully converted to bitcoin. Most recently in June 2021, there was further non convertible debt issued, using the proceeds to purchase yet more bitcoin.

Some numbers for context. As of the time of this writing (August 5, 2021):

MicroStrategy HODLs 105,085 BTC worth a total of approx $4.1B (purchased at an average price of $26,080 per coin). The MSTR share price is currently $666, with a total company value of approx $6.5B. Their situation is unparalleled amongst other companies in terms of both:

- their bitcoin holdings as a percentage of their company value or market cap

- the overall size of the company.

In other words, other large companies (such as Tesla) hold much smaller percentages of bitcoin relative to company size, whereas other high percentage holders are simply far smaller in size.

These numbers can be seen at the following chart of bitcoin treasuries in publicly traded and private companies.

Starting around August of 2020, we began to see bitcoin being added to the balance sheets of public companies. One such company is MSTR. This is why you often hear MSTR described as a proxy Bitcoin ETF. However, it’s a more dynamic situation than that due to their likely ongoing BTC buys in the future. Hence why I’m looking at how a traditional value investor might value them.

Traditional Dollar-Based Valuation

First, the way the market will mainly be valuing MSTR is in dollar terms. After all, the share price is priced in dollars and profits are made in dollars.

For those unfamiliar, I’m going to explain how this type of valuation might be formed step by step.

MSTR makes fairly stable profits and have not grown significantly in recent years.. The most conventional way of valuing a company like this is to sum up the present value of all of estimated future profits, and then to add in any other relevant assets aside from this, like bitcoin.

What do we mean by present value? $100 received in 10 years time is not as valuable as $100 right now , so we need to discount future profits by an interest rate to derive the value now.

For example, we might value $100 in 10 years as: $100 / 1.0122 ^ 10 = $88.60

The interest rate used here is the 10-year return on U.S. treasuries, seen as the “risk-free” rate of return on U.S. dollars. Treasuries are considered near risk free because if it ever came to it, the Fed could create more dollars to pay the obligation.

In other words, if we want $100 in 10 years, we can invest $88.60 now to return it. Conversely we can say that the prospect of being paid $100 in 10 years is “worth” $88.60 to us now. We can then repeat this calculation every year to “discount” all expected future profits and sum them all up. This method of valuation is particularly analogous to valuing companies paying dividends, since these profits get paid out to shareholders as cash flow streams. It’s pretty similar to the method of valuing a bond too.

As it happens, historically MicroStrategy did not pay out profits as dividends, but built up a large cash pile on their balance sheet, which is what led Michael Saylor to consider bitcoin in the first place. Whether dividends are actually paid out, put on the balance sheet, or reinvested in the business, it is the underlying ability to generate profits which underpins the basis of value investing.

In reality, analysts use a much higher interest rate in their calculation for valuing shares than the risk free rate. The overall interest rate used might reflect the risk free treasury rate for the period in question plus an additional “equity risk premium”. The latter reflects the fact that future profits are much less certain to be realised than nominal returns in U.S. treasuries, which are seen as risk free. This premium is highly subjective but may sit at about 5–6% per annum. for US Equities on average. .

All told, the current MSTR market cap of $6.5B reflects current bitcoin holdings worth $4.1B, plus the present value placed on the discounted sum of all future profits, along with other factors. These might include any positive or negative premium placed on MSTR by the market, and also an adjustment for the convertible debt issued, as to whether these are likely to be converted to equity at future dates.

In June 2021 there was a further bond issue announced, and yet another illustration of MSTR being in a dynamic situation and acquiring more bitcoin when the opportunity presents. This latest bond issue is not convertible. It has been used to buy more bitcoin now, but will reduce their capacity to convert future profits to bitcoin as they will have to pay these bond coupon payments as a priority. To illustrate this, the issue is $500m at an annual interest rate of 6.125%, so the company will have to pay around $30.6m each year to service the interest payments.

Bitcoin Based Valuation

I think there is now a slight issue with the conventional way of valuing MSTR in dollar terms. It relates to the “opportunity cost” of buying MicroStrategy shares.

Every time we invest in an asset, we forgo the use of that money somewhere else — this is called the opportunity cost. But where else might we hold that money? There is no way anyone is investing in MSTR now without being a believer in the substantial bitcoin held by them as a longer-term investment. Arguably, by investing in MicroStrategy one is mainly foregoing a “risk free” investment in bitcoin itself that they could otherwise hold. The logical result is to try and price MSTR in BTC instead! And in doing so, evaluate whether the MSTR investment is “worth” the bitcoin invested, versus the risks.

It’s worth noting that there are stakeholders out there for whom the only exposure to bitcoin permitted them is buying shares in a company such as MSTR. While this may be significant for some, let’s assume otherwise for now.

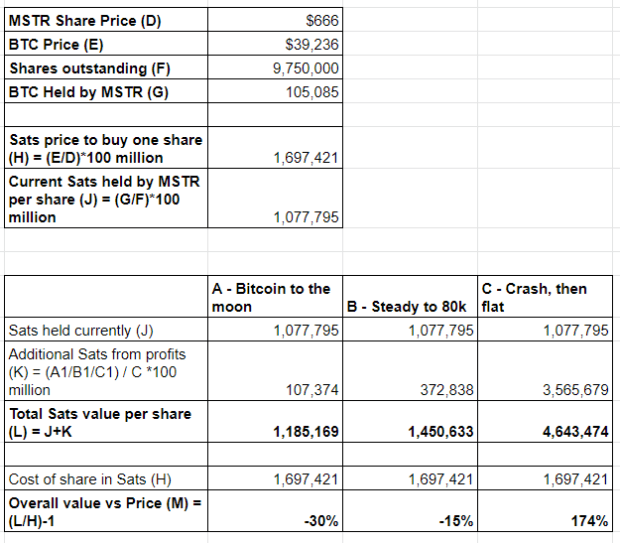

So how do we price MSTR in bitcoin? The starting point is simple: MicroStrategy holds 105,085 bitcoin right now.

We then need to add on a present value of all the bitcoin they might accumulate in the future. This is clearly the tricky part, as profits are in dollar terms, so we have to estimate how the bitcoin price in dollars might move over time. We also have to estimate the future profits of the company (same as before).

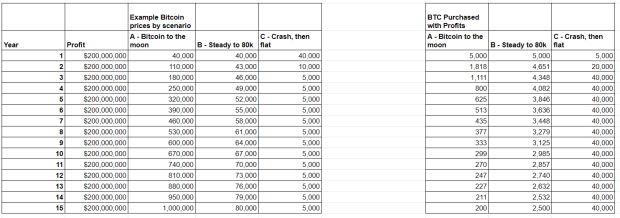

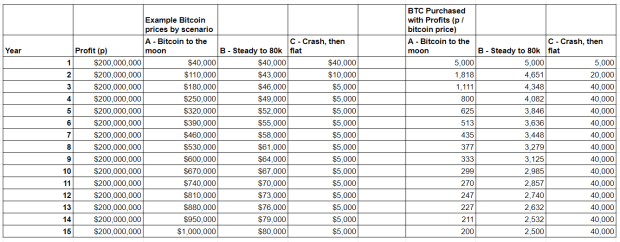

This article is focused more on the concept than the practice. I’m certainly not going to model either with any precision! However, I’ve made up some far-out scenarios to illustrate. In regard to profits converted to bitcoin, others are far better qualified to dig through the accounts, but for the purposes of this illustration let’s assume MSTR converts $40M worth of profits to bitcoin each quarter and that this continues for 15 years. All highly subjective.

How would we discount these profits? Holding BTC doesn’t offer a risk-free return, so we don’t have to use a treasury rate as above — we in effect use 0%.

However, the equity risk premium part referred to above should still stand. This again reflects the uncertainty of making an equity investment, in this case, versus simply holding the underlying risk-free bitcoin. Remember, it’s termed “risk free” in BTC terms.

Finally, we need prices of conversion to BTC. I’d view any stochastic analysis as simply impossible to get right! To keep things simple, let’s deterministically apply three scenarios for the next 15 years for an illustration:

a) “To the moon” — bitcoin hitting $1M per bitcoin in 15 years time.

b) “Slow and steady” — achieving growth of under 5%% per annum to hit $80,000 per bitcoin in 15 years.

c) “False dawn” — a swift retreat down to $5,000 per bitcoin after this year and remaining at this level, supported only by hardcore HODLers from then on.

These are deliberately differing scenarios. The screenshot below shows — in theory — how much BTC might be purchased in each year for each scenario.

Do not take these numbers seriously!

So how would we evaluate an investment of bitcoin into MSTR today?

To keep the illustration simple, let’s consider one share of MSTR and try to value this single share in bitcoin,in terms of the bitcoin MSTR holds now, plus future profits converted to bitcoin.

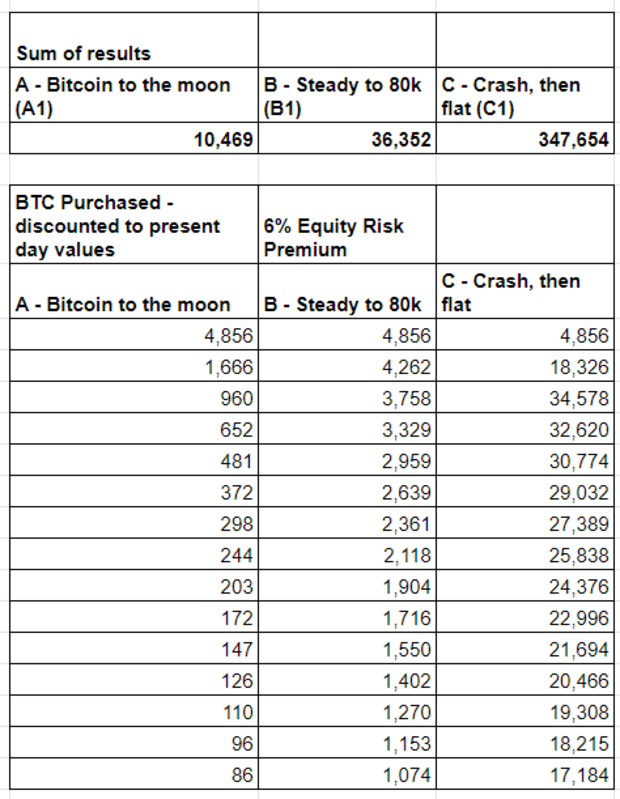

We then need to discount the additional future BTC buys from the table above, and add the sum of those to this too. So:

- We converted the assumed annual USD profits at the broad brush rates in each scenario (see table above);

- discount using the equity risk premium only to obtain the present values of future bitcoin purchases (see table below); and

- add the existing bitcoin that MSTR hold.

Summing these then provides an estimate of future bitcoin MSTR purchases under each scenario.

The question:“if we invest one bitcoin into MSTR shares, will we make a positive return on that when we value those shares in bitcoin?”

As shown above, when we compare the overall value of sats that one share of MSTR might generate to the current price in SATs, we see the following returns –

a) -30%

b) -15%

c) +174%

Based on scenario A, it might be a hard sell to invest your bitcoin into MSTR. Scenario B is close to par, and scenario C actually looks like a good payoff in BTC terms.

The most striking thing about these results becomes obvious when you think about it. The worse bitcoin performs over the 15-year period, the better an investment MSTR looks when valued in BTC! This is as MSTR will acquire more BTC at a lower bitcoin price for the dollar profits it makes.

Many thanks for early comments on this article from @YATReviews on Twitter, who has pointed out this outcome is consistent with viewing MSTR as a “bitcoin dividend security”. For normal dividend stocks valued in dollars, their dividends (if consistent) can actually prove more powerful at compounding wealth when the share price is low, since those dividends purchase more shares.

The other point to note is that if BTC does very well in the coming years, at the present size of the business MSTR may not move the dial that much in terms of adding to their holdings (see scenario A, where only around 10% more bitcoin is added to current holdings from future profilts).).

Some large disclaimers: as already mentioned, no allowance is currently made of the convertible bonds issued which can be converted to equity. My understanding is that the first offer had a conversion rate of $398 for 1.6M shares; a simple method is to include these on the number of shares in the valuation, if not included already. The second offering is at $1,432, so this is more complex to price. I would love any feedback on simple ways to include them. Also, there is the most recent “straight up” bond issue from June 2021which is not convertible. Whilst we have assumed slightly lower profits converted to bitcoin due to the $30m annual coupon payments, we should also allow for the repayment of the $500m principal at expiration.

Final Thoughts

Why might this change of valuation method to value in bitcoin prove relevant?

Preston Pysh has previously commented on this. Imagine we were to move to an increasingly bitcoin denominated world in which bitcoin continues to appreciate and more and more companies hold bitcoin on their balance sheets.

Individuals with bitcoin would still make investments, but only if the potential of these investments outweigh the opportunity cost of just holding bitcoin instead. This might lead back to “value” equities performing well again, as entities generating profits can add more bitcoin to their balance sheets. Conversely, companies not generating free cashflows can’t, and hence their valuations when priced in bitcoin might be lower..

It might be said that the current trend to invest in growth equities results from everyone having a pretty high time preference — and hence not valuing future dividends as much. Bitcoin reduces time preference and hence might change this. For the concept to really resonate, future profits would be realized (or at least easily valued) in bitcoin. For now, it is only really bitcoin miners for whom this type of calculation can be made, (Adam Back has commented on this too) but even they have fiat denominated costs.

I would love any thoughts or feedback on this article — especially ideas on the valuation concepts discussed. Please note all of this is painted with an incredibly broad brush — the numbers not intended to be accurate — and this is more of a thought experiment than hard quantitative analysis

Disclaimer — the author owns both bitcoin and shares in MSTR. This article should not be taken as an endorsement to buy either.

Exploring the world of Bitcoin on Twitter @bitcoinactuary.

This is a guest post by BitcoinActuary. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc. or Bitcoin Magazine.