- May 18, 2023

- Posted by: admin

- Category: BitCoin, Blockchain, Cryptocurrency, Investments

No Comments

Quick Take

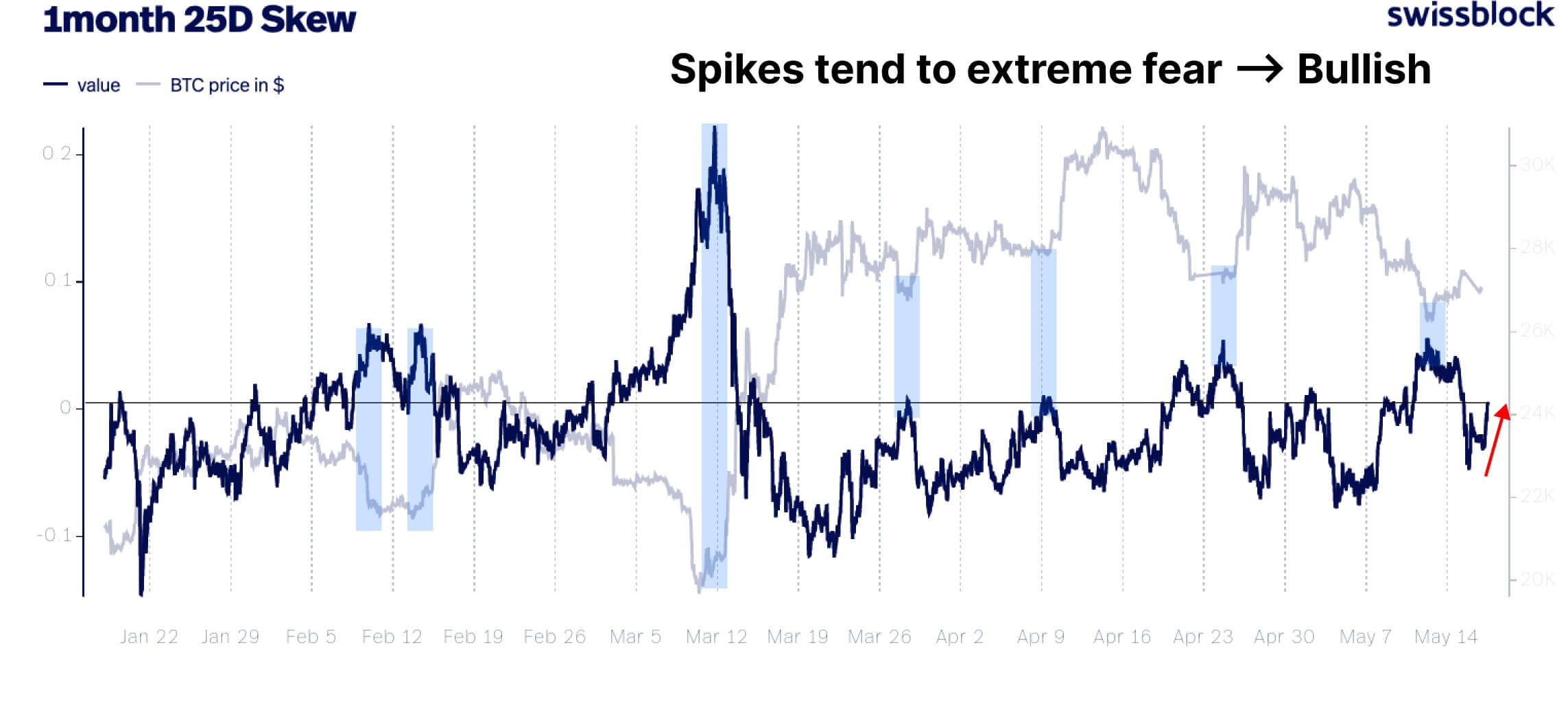

- Skew is the relative richness of put vs call options, expressed in terms of Implied Volatility (IV). For options with a specific expiry, 25 Delta Skew refers to puts with a delta of -25% and calls with a delta of 25% to demonstrate this difference in the market’s perception of implied volatility.

- The Bitcoin 1-month 25D Skew suggests a “Put Premium”; the demand for puts increases as investors seek coverage to the downside.

- However, across the entire curve, the put-to-call ratios’ overall position in the options market is skewed to the upside.

- This has been a bullish indicator this year.

A breakdown of the curve

- 1 Week: -0.496%

- 1 Month: -0.293%

- 3 Months: -0.212%

- 6 Months: -3.156%

The post Bitcoin 1-month 25D Skew suggests a “Put Premium” appeared first on CryptoSlate.