- June 21, 2022

- Posted by: admin

- Category: BitCoin, Blockchain, Cryptocurrency, Investments

Many cryptocurrency lending schemes are eerily similar to banks’ abilities to loan out money and create debt through fractional reserve banking.

Margarita Groisman graduated from the Georgia Institute of Technology with a degree in industrial engineering and analytics.

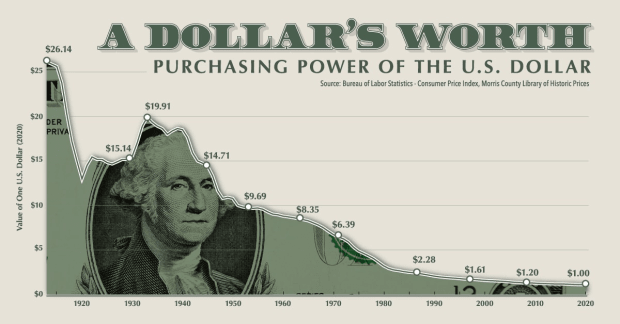

Since modern capitalism’s emergence in the early 19th century, many societies have seen a meteoric rise in wealth and access to cheap goods — with the party coming to an end years later with some sort of major restructuring triggered by a major world event, such as a pandemic or a war. We see this pattern repeat again and again: a cycle of borrowing, debt and high-growth financial systems; then what we now call in America “a market correction.” These cycles are best explained in Ray Dalio’s “How The Economic Machine Works.” This article aims to examine whether a new monetary system backed by bitcoin can address our systematic debt issues built into the monetary system.

There are countless examples in history to illustrate the long-term problem with using debt and money printing to solve financial crises. Japan’s inflation following World War II due to printing monetization of fiscal debt, the eurozone debt crisis, and what seems to be starting in China, beginning with the Evergrande crisis and real estate market collapse in prices and unfortunately, many, many more cases.

Understanding Banking’s Reliance On Credit

The fundamental problem is credit — using money you don’t have yet to buy something you can’t afford in cash. We will all likely take on a large amount of debt one day, whether it’s taking on a mortgage to finance a house, taking on debt for purchases like cars, experiences like college, and so on. Many businesses also use large amounts of debt to conduct their day-to-day business.

When a bank gives you a loan for any of these purposes, it deems you as “credit-worthy,” or thinks that there is a high chance your future earnings and assets combined with your record of payment history will be enough to cover the current cost of your purchase plus interest, so the bank loans you the rest of the money needed to purchase the item with a mutually-agreed upon interest rate and repayment structure.

But where did the bank get all that cash for your large purchase or the business activities? The bank doesn’t manufacture goods or products and is therefore generating extra cash from these productive activities. Instead, they also borrowed this cash (from their lenders who chose to put their savings and extra cash in the bank). To these lenders, it may feel as if this money is readily available for them to withdraw at any moment. The reality is that the bank loaned it out long ago, and charged interest fees significantly more than the interest they pay out to cash deposits, so they can profit from the difference. Furthermore, the bank actually loaned out much more than lenders gave them on the promise of using their future profits to pay back their lenders. Upon a saver’s withdrawal, they simply move around someone else’s cash deposit to ensure you can pay for your purchase right away. This is obviously an accounting oversimplification, but essentially is what happens.

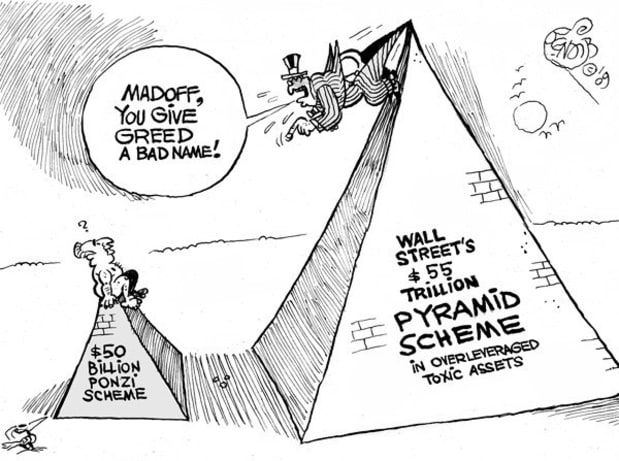

Fractional Reserve Banking: The World’s Biggest Ponzi Scheme?

Welcome to fractional reserve banking. The reality of the money multiplier system is that on average, banks loan out ten times more cash than they actually have deposited, and every loan effectively creates money out of thin air on what is simply a promise to pay it back. It is often forgotten that these private loans are what actually creates new money. This new money is called “credit” and relies on the assumption that only a very small percentage of their depositors will ever withdraw their cash at one time, and the bank will receive all their loans back with interest. If just more than 10% of the depositors try to withdraw their money at once —for example, something driving consumer fear and withdrawal or a recession causing those who have loans not being able to repay them — then the bank fails or needs to be bailed out.

Both of these scenarios have occurred many times in many societies that rely on credit-based systems, though it might be useful to look at some specific examples and their results.

These systems basically have a built-in failure. At some point, there is a guaranteed deflationary cycle where the debt must be paid back.

Society Pays For The Bank’s Risky Loans

There is a lot to discuss in terms of how the central bank attempts to stop these deflationary cycles by decreasing the cost for businesses to borrow money and adding newly-printed money into the system. Fundamentally though, short-term solutions like this cannot work because money cannot be printed without losing its value. When we add new money to the system, the fundamental result is that we are transferring the wealth of every individual in that society to the bleeding bank by decreasing the spending power of the entire society. Essentially, that is what happens during inflation: Everyone, including those not originally involved in these credit transactions, gets poorer and has to pay back all the existing credit in the system.

The more fundamental problem is a built-in growth assumption. For this system to work, there must be more students willing to pay for the increasing costs of college, more people looking to deposit and get loans, more home buyers, more asset creation and constant productive improvement. Growth schemes like this don’t work because eventually the money stops coming and individuals don’t have power to effectively transfer the spending power of the population to pay these debts like banks do.

The system of credit has brought many societies and individuals into prosperity. However, every society that has seen true long-term wealth generation has seen that it comes through the creation of innovative goods, tools, technologies and services. This is the only way to create true long-term wealth and bring about growth. When we create products that are new, useful and innovative that people want to buy because they improve their lives, we get collectively wealthier as a society. When new companies find ways to make goods we love cheaper, we get collectively wealthier as a society. When companies create amazing experiences and services like making financial transactions instant and easy, we get collectively wealthier as a society. When we try to create wealth and massive industries that rely on using credit to bet on risky assets, make market trades and make purchases beyond our current means, then society stagnates or places itself on a trajectory toward decline.

Would it be possible to move toward a system with a more long-term focused outlook with slower but steady growth without the pain of extreme deflationary cycles? First, extreme and risky credit would need to be eliminated which would mean much slower and less short-term growth. Next, our never-ending cash printer would need to end which would lead to extreme pain in some areas of the economy.

Can Bitcoin Address These Issues?

Some say that bitcoin is the solution to these problems. If we move to a world where bitcoin is not just a new form of commodity or asset class, but actually the foundation of a newly-decentralized financial structure, this transition could be an opportunity to rebuild our systems to support long-term growth and end our addiction to easy credit.

Bitcoin is limited to 21 million coins. Once we reach the maximum bitcoin in circulation, no more can ever be created. This means that those who own bitcoin could not have their wealth taken from the simple creation of new bitcoin. However, looking at the lending and credit practices of other cryptocurrencies and protocols, they seem to mirror our current system’s practices, but with even more risk. In a newly-decentralized monetary system, we must make sure we limit the practice of highly-leveraged loans and fractional reserves and build these new protocols into the exchange protocol itself. Otherwise, there will be no change from the issues around credit and deflationary cycles as we have now.

Cryptocurrency Is Following The Same Path As Traditional Banking

It is simply really good business to loan out money and guarantee returns, and there are numerous companies in the cryptocurrency ecosystem making their own products around highly risky credit.

Brendan Greeley writes a convincing argument that loans cannot be stopped just by switching to cryptocurrencies in his essay “Bitcoin Cannot Replace The Banks:”

“Creating new credit money is a good business, which is why, century after century, people have found new ways to make loans. The U.S. historian Rebecca Spang points out in her book ‘Stuff and Money in the French Revolution’ that the monarchy in pre-revolutionary France, to get around usury laws, took lump-sum payments from investors and repaid them in lifetime rents. In 21st-century America, shadow banks pretend they are not banks to avoid regulations. Lending happens. You can’t stop lending. You can’t stop it with distributed computing, or with a stake to the heart. The profits are just too good.”

We saw this happen just recently with Celsius as well, which was a high-yielding lending product that did essentially what banks do but to a more extreme degree by lending out significantly more cryptocurrency than it actually had with the assumptions that there would not be a large amount of withdrawals at once. When a large amount of withdrawals occurred, Celsius had to halt them because it simply did not have enough for its depositors.

So while creating a set limited supply currency may be an important first step, it doesn’t actually solve the more fundamental problems, it just cuts out the current anesthetics. The next step towards building a system around long-term and stabilized growth, assuming future use of an exchange, is standardizing and regulating the use of credit for purchases.

Sander van der Hoog provides an incredibly useful breakdown around this in his work “The Limits to Credit Growth: Mitigation Policies And Macroprudential Regulations To Foster Macrofinancial Stability And Sustainable Debt?” In it, he describes the difference between two waves of credit: “a ‘primary wave’ of credit to finance innovations and a ‘secondary wave’ of credit to finance consumption, overinvestment and speculation.”

“The reason for this somewhat counter-intuitive result is that in the absence of strict liquidity requirements there will be repeated episodes of credit bubbles. Therefore, a generic result of our analysis seems to be that a more restrictive regulation on the supply of liquidity to firms that are already highly leveraged is a necessary requirement for preventing credit bubbles from occurring again and again.”

The clear boundaries and specific credit rules that should be put in place are outside of the scope of this work, but there must be credit regulations put into place if there is any hope of sustained growth.

While van der Hoog’s work is a good place to start to consider more stringent credit regulation, it seems clear that normal credit is an important part of growth and is likely to net positive effects if regulated correctly; and abnormal credit must be heavily limited with exceptions for limited circumstances in a world run on bitcoin.

As we seem to be gradually transitioning into a new currency system, we must make sure that we don’t take our old, unhealthy habits and simply convert them into a new format. We must have built-in stabilizing credit rules right into the system, or it will be too difficult and painful to transition out of the dependence on easy cash — as it is now. Whether these be built into the technology itself or in a layer of regulation is yet unclear and should be a topic of significantly more discussion.

It seems that we have come to simply accept that recessions and economic crises will just happen. While we will never have a perfect system, we may indeed be moving toward a more efficient system that promotes long-term maintainable growth with the inventions of bitcoin as a means of exchange. The suffering caused to those who cannot afford the inflated price of necessary goods and to those who see their life savings and work disappear during crises that are clearly predictable and built into existing systems do not actually have to occur if we build better and more rigorous systems around credit in this new system. We must make sure we don’t take our current nasty habits that cause extraordinary pain in the long term and build them into our future technologies.

This is a guest post by Margarita Groisman. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc. or Bitcoin Magazine.